← Back to blog index · 2026-05-10

Bitfinex Funding Period Selection — 2/7/30/120 Days Analyzed With Real 2026 Data

Complete trade-off analysis for the 4 Bitfinex Funding period buckets. Real APR distributions from 2026, prepayment risk, when to pick which. Boxplot + decision matrix included.

Bitfinex Funding lets you choose lending periods from 2 to 120 days. Most people default to 2 days because “shorter feels safer”.

That’s usually wrong. Locking longer typically earns more — you just need to know when to lock long and when to stay short. This post explains the trade-offs with real 2026 data.

TL;DR

- Short (2d): lower APR (median 3-6%), best for capturing spikes and rotating fast

- Mid (7d): balanced default (median 5-7%), most-used preset

- Long (30d): higher APR (median 7-10%), but exposure to prepayment shortening

- Xlong (120d): highest nominal APR (median 8-13%, spike-mode 25%+), highest prepayment risk

- Multi-bucket diversification typically beats single-period by 1-3pp APY

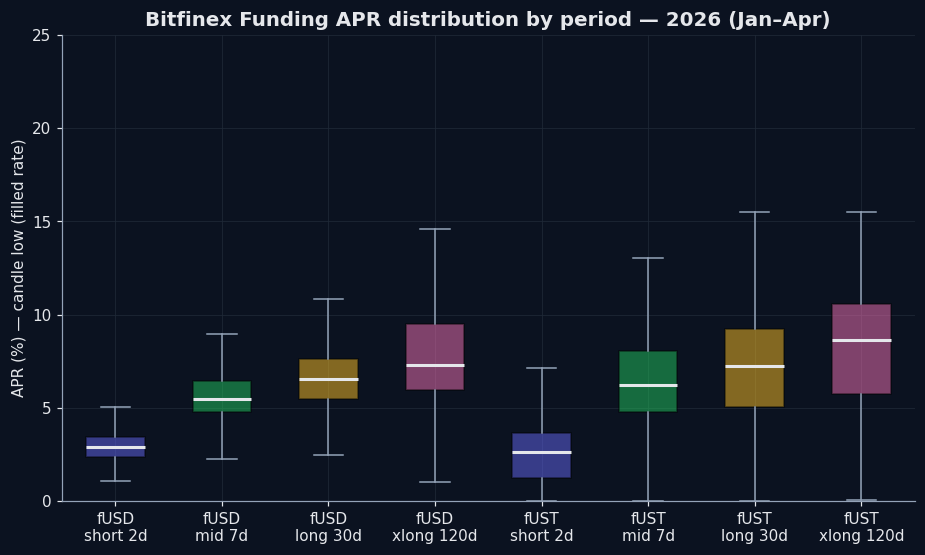

The 4 Buckets — Real APR Distributions

Box plot below uses Bitfinex 2026 Q1 public candle data. Each box shows the 25-75 percentile range of “candle low” (= filled rates) per bucket.

Key observations:

- fUSD systematically pays more than fUST by 1-2pp on average (USDT is the dominant collateral)

- APR scales with period as theory predicts, but fUST long periods (30d/120d) have higher dispersion

- 120d xlong upper tail is extreme, but the median isn’t far above 30d — most of the time the gap is small

Why Longer Periods Pay More

It’s a borrower premium:

- Borrower locks 2 days → if rates rise, they renegotiate quickly. Low risk → low premium.

- Borrower locks 120 days → stuck for 4 months. If rates spike to 50% during that window, they still pay 13%. They want compensation upfront.

Empirical: Bitfinex’s public funding data shows 2026 fUSD 120d averaging 4-7pp above 2d.

Real Use Cases for Each Period

Short 2d — “The Capture-er”

APR median: fUSD 5-6%, fUST 3-4% (2026) Use when:

- Rates are climbing → lock 2d, re-price upward at expiry

- You expect cooling → don’t get stuck at current low rate

- High liquidity needs → 2d is the shortest lock available

Avoid when:

- Markets are flat → APR too low, no spike capture upside

- You want full automation → 2d is the highest re-quote frequency

Mid 7d — “The Default”

APR median: fUSD 6-8%, fUST 5-7% Use when: Most of the time. Mid is the steady sweet spot — not stuck too long, reasonable rate, prepayment risk manageable.

Avoid when: Rates are clearly trending (up or down).

Long 30d — “The Steady Earner”

APR median: fUSD 8-12%, fUST 7-10% Use when:

- Funding environment looks stable for ~1 month → lock long for higher rate

- Want to reduce operations → 30d locks once, expires at month-end naturally

Avoid when:

- Rates clearly falling → don’t lock 30 days at 8% while spot drops to 4%

- Expecting BTC volatility → margin users will deleverage, prepayment risk spikes

Xlong 120d — “The Insurance + Yield Play”

APR median: fUSD 12-15%, fUST 8-13% (spike-mode 25-50%) Use when:

- During spikes — lock 12-15% rate for 4 months, even when market cools you keep earning

- As insurance — even if spot APR drops to 1%, your 120d portion is locked at 13%

Avoid when:

- Capital may be needed — 4 months is real; prepayment helps but can’t be counted on

- < $1K capital — opportunity cost of locking too high

Prepayment Risk — The Hidden Cost of Long Periods

Most newcomers miss this: borrowers can repay early. Your 120d loan might return in 30 days.

What actually happens:

- Borrower repays → principal lands back in your wallet, interest prorated

- You expected 120d × 13% = 4.27% return; you might only get 30d × 13%/12 = 1.07% (then have to redeploy)

Full prepayment hazard analysis has detailed survival curves. Quick summary:

- Calm market → 120d loans typically survive 80-100 days

- BTC volatility regime → 120d loans can drop to 30-60 days (deleverage cascades)

So the “high nominal APR” of long buckets needs a prepayment discount applied to get true expected yield.

Multi-Bucket Diversification — Why 4 Buckets at 25% Each Often Wins

I did a detailed multi-bucket vs single comparison. The headline:

Single 30d strategy in 2026 simulation: avg APY 7.65%

4-bucket equal-weight, same period: avg APY 9.2%Why? Multi-bucket captures spikes without single-period lock-in. Short (2d) keeps recycling to grab spikes; xlong (120d) holds during crashes locking in high rates.

What Should You Pick

If you run manually:

- Capital < $5K → all 7d (default, lowest ops)

- Capital $5K-$50K → 50% 7d + 30% 30d + 20% 2d (balanced)

- Capital > $50K → 4-bucket diversified (25% each, periodic rebalance)

If you use a bot (e.g. Yieldsforge):

- Pick balanced preset → auto 4-bucket diversification + per-symbol floor tuning

- Don’t think about period — the bot evaluates every 60 seconds

Related Reading

- How Bitfinex Funding APR Works — all the mechanics beyond period

- FRR vs Limit Orders — Which to Use

- Prepayment Hazard — The Hidden Cost

- Multi-Bucket vs Single-Period Comparison

- Why Bitfinex Funding Beats DeFi Yields — the hub

Disclosure: I’m the developer of Yieldsforge. APR data sourced from Bitfinex public candle data, 2026-01 to 2026-04. Not investment advice.