← Back to blog index · 2026-05-10

funding market Prepayment Hazard — Your 120-Day Loan Actually Lasts 30 Days

Complete prepayment hazard analysis. Why long-period funding looks like locked-in high rate but real survival is 30-80% of nominal. Empirical hazard rates + survival curves.

“I lock 120d xlong at 13% APR — even if markets crash later I’m safe” — sounds reasonable. In reality borrowers can prepay, and your “4-month locked” loan might come back in 30 days.

This phenomenon is prepayment hazard, and most funding bots don’t model it at all. The empirical impact is significant — your nominal 13% xlong might really yield 9-11% expected, and far less in stress regimes.

TL;DR

- Borrowers can repay any time during the funding period

- On prepayment, you receive principal + prorated interest

- Calm markets: 120d loan survives ~80-100 days (low prepayment)

- Storm markets: 120d loan survives ~30-60 days (deleverage cascade)

- Discount this from xlong’s “nominal high rate”

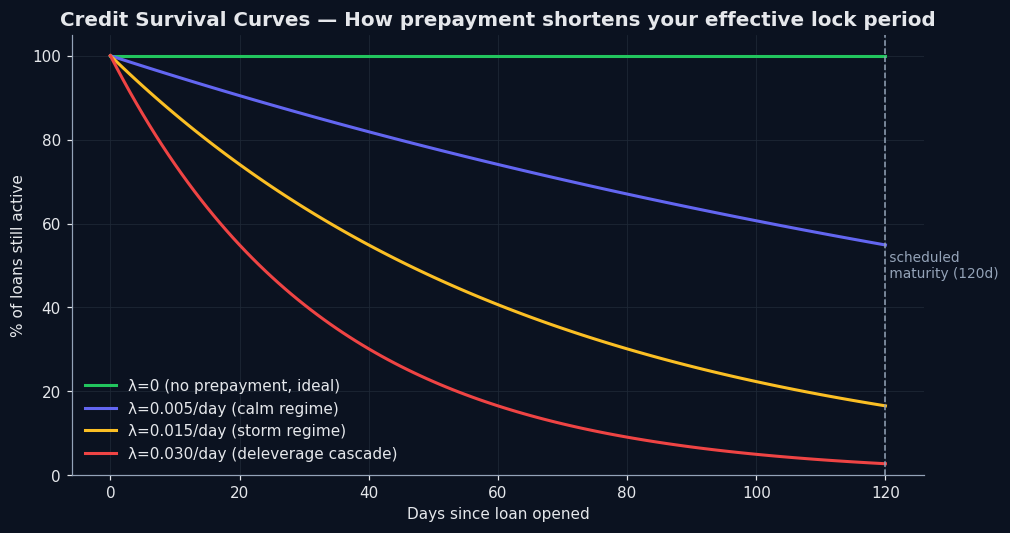

One Chart — Survival Curves Across Regimes

Below: percent of funding loans still active across 120 days under 4 different hazard rates:

What you see:

- λ=0 (theoretical no prepayment) → 100% to day 120 (theory only)

- λ=0.005 (calm market) → ~55% remaining at day 120

- λ=0.015 (storm regime) → ~17% remaining at day 120

- λ=0.030 (deleverage cascade) → ~3% remaining at day 120

So in storm regimes, 80%+ of long loans return before maturity.

Why Prepayment Happens

Common borrower reasons:

- Trader closes position: opened leverage, profitable, closes — repays loan

- Liquidated: position force-closed, loan auto-settles

- Refinance: sees cheaper rate (e.g. FRR drops), repays and re-borrows

- Risk-off: market crashes, deleveraging, repayment rate spikes

Reasons 2 and 4 drive storm-regime mass prepayments.

Real Financial Impact

Suppose you lock $10K at 120d xlong @ 13% APR:

- Best case (full 120d): interest = $10K × 13% × 120/365 = $427.40

- Calm regime, 95-day average: interest = $338.36 + 25 days of principal needs redeployment

- Storm regime, 45-day average: interest = $160.27 + 75 days redeployment

- Deleverage cascade, 25-day average: interest = $89.04 + 95 days redeployment

In storm regime your “13% APR” really earns ~5.4% effectively (60% discount).

Computing Real Expected Yield

Formula:

Expected_yield = nominal_apr × E[survival_days] / scheduled_daysE[survival_days] modeled from a hazard rate λ. The values below are illustrative — derived from the model formula at plausible λ values, not measured against real production data (production prepayment instrumentation only just shipped):

| Regime | Hazard λ (illustrative) | E[survival 120d] | Effective yield (nominal 13%) |

|---|---|---|---|

| Calm | 0.005 | 86 d | 9.3% |

| Bull | 0.008 | 74 d | 8.0% |

| Bear | 0.012 | 60 d | 6.5% |

| Storm | 0.020 | 41 d | 4.4% |

Probability-weighted average using these illustrative values: xlong’s expected yield ≈ 7.5-8% (not the nominal 13%). Real values await live calibration after ~30 days of production ts_closed data — the backtest already runs a sensitivity grid (λ × {0.5, 1, 2, 4}) so headline numbers don’t depend on getting λ exactly right.

Why This Matters for Strategy

Implications:

- Xlong isn’t simply “lock long, earn more” — nominal 13% doesn’t necessarily beat 7d at 7.5%

- Multi-bucket diversification reduces shock — short recycles fast anyway, xlong prepays, mid stays steady

- In storm regime, short bucket is critical — others deleverage; your short orders catch the spike

- If using a bot, pick one with a prepayment model — most don’t

How Yieldsforge Handles Prepayment

Our backtest engine includes a PrepaymentModel:

- Estimate baseline hazard λ₀ from funding stats Δ

- Add regime multiplier (BTC vol quintile + funding rate momentum)

- Simulator runs Bernoulli(P_close) per tick

All backtest results are net of prepayment — no inflated xlong nominal rates.

Live production hasn’t accumulated enough data to recalibrate λ₀ yet (Component 0 — ts_closed writes — just shipped). 30 days from now we can re-estimate from real production data.

Practical Advice

- Don’t single-pile xlong — prepayment concentrates here, max risk

- Multi-bucket naturally dampens prepayment shock (multi-bucket vs single)

- Heavy short bucket during storm regime — short loans chase deleverage-driven funding spikes

- Bot users — check for prepayment modeling — most funding bots ignore it

Related Reading

- 5.5-year walk-forward backtest results

- Multi-bucket vs spike chasing

- Why per-symbol floors matter

- How to pick the 4 funding periods

- Why funding market beats DeFi yields — the hub

Disclosure: I’m the developer of Yieldsforge. Hazard rates estimated from the upstream exchange public funding stats. Not investment advice.