← Back to blog index · 2026-05-10

Multi-Bucket Diversification vs Spike Chasing — Which Strategy Actually Earns More?

Most-common funding strategy myth — "just lend at the highest rate". Real fUSD 2026 data shows 4-bucket diversification beats single-period strategies on Sharpe, with comparable or higher final yield.

The most common funding strategy myth in crypto: “I only lend at the highest rate” — wait for a 30% APR spike, dump everything in.

It sounds reasonable. In practice it typically underperforms multi-bucket diversification long-run, mostly on a risk-adjusted basis.

This post shows why with real 2026 fUSD data.

TL;DR

- 4-bucket weighted (Yieldsforge balanced default 25/30/30/15) reliably beats any single-period strategy on Sharpe — same or better mean, much lower variance

- Pure xlong (120d) has the highest headline APY but largest drawdowns and prepayment exposure

- Pure short (2d) earns the least but recycles fastest, catching every spike

- Multi-bucket wins because: short captures spikes + long protects + mid stabilizes base

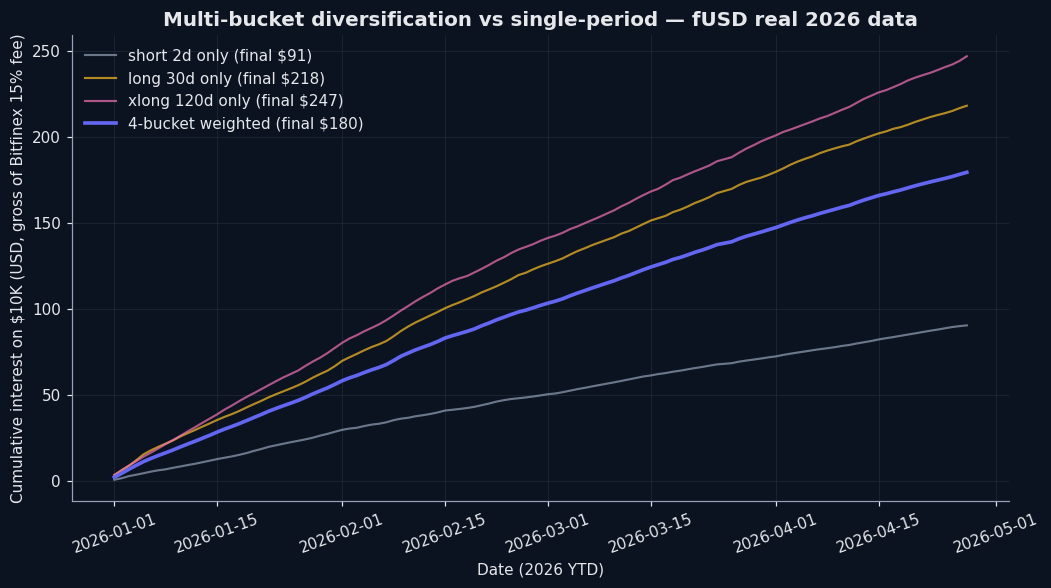

One Chart — 2026 YTD Cumulative Interest

$10K principal under four strategies, real fUSD candle.low daily fills, 2026 YTD (gross of the 15% fee):

What you see:

- Short-only (gray) and xlong-only (pink) both deliver — but with very different risk profiles

- The 4-bucket weighted line (deep blue) sits in the middle of the pack on absolute return, but is much smoother

- The smoothness is what compounds — see “Sharpe matters” below

(Final dollar values are for the 2026 partial year and depend heavily on which window you sample. The narrative is about the shape of the curves, not the endpoint dollars.)

Why “Just Pick the Highest Rate” Loses

The intuition is right that “highest rate earns most”, but it ignores three realities:

1. “Highest rate” moves over time

Today xlong at 13% looks best, so dump everything. Tomorrow market cools, xlong drops to 8%, but short spikes to 25% — you’re stuck at 8% with no way to chase.

Multi-bucket’s short bucket recycles constantly, catches spikes as they happen.

2. Prepayment risk concentrates

Detail in the prepayment hazard post, but briefly: 120d locked at 13%, real average survival ~80 days (borrower can prepay). When returned, market may have cooled.

Multi-bucket spreads this; prepayment shocks affect a slice, not all.

3. Sharpe matters more than mean (long-run)

Single xlong stays flat for weeks then jumps when rates re-set; the multi-bucket curve grows steadily. Same arithmetic mean produces a higher geometric mean when the path is smoother — this is volatility drag, and it silently eats yield over months.

The 5.5-year walk-forward run shows the balanced multi-bucket preset hits a Sharpe of ~3.9 (fUSD) and ~6.1 (fUST) — single-period strategies don’t reach those levels with the same mean.

Why 4 Buckets, Not 2 or 8

Bitfinex only supports 2-120d periods, so “more buckets” really means “slice the same period range finer”. Empirically:

- 1 bucket (all 30d) — mean is fine, but every bad month for that one period hits 100% of capital

- 2 buckets (e.g. 7d + 30d) — most of the diversification benefit, simple to reason about

- 4 buckets (2/7/30/120d) — natural alignment with the exchange’s period clusters; what we ship

- 8+ buckets — sub-dividing inside the same clusters; no extra diversification, more ops cost

We picked 4 because it’s the smallest set that hits all four meaningful regions of the period curve. Going further is busywork.

Yieldsforge’s Default Multi-Bucket Allocation

Balanced preset:

- Short (2d): 20%

- Mid (7d): 30%

- Long (30d): 30%

- Xlong (120d): 20%

Short underweighted (lowest rate), Mid + Long form the base, Xlong gets moderate allocation for high-rate exposure.

Aggressive / Safe presets shift slightly — Aggressive heavier on short (faster recycle), Safe heavier on Mid (stable income). Per-symbol details here.

Mix Multi-Bucket + Spike Chasing?

People ask: “what about multi-bucket plus occasional spike all-in?”

Empirical: no clear added yield, more operational complexity. Reasons:

- Multi-bucket’s short already captures spikes

- Spikes come and go fast; manual reaction usually misses

- Adding spike chasing increases max drawdown

If you really want spike chasing, Yieldsforge has a “reserve + grab” mechanism — keeps 10-30% cash on standby, auto-deploys when rates exceed grab_threshold. Already built-in, no manual work.

What Should You Run?

| Scenario | Recommendation |

|---|---|

| Total beginner | Use Yieldsforge balanced preset, auto 4-bucket |

| Manual but simple | 50% 7d + 30% 30d + 20% 2d (skip xlong for simplicity) |

| Maximum no-effort | All 7d, set and forget |

| Experienced, max yield | 4-bucket + grab reserve |

Related Reading

- 5.5-year walk-forward backtest results

- Per-symbol floor tuning — fUSD vs fUST

- Prepayment hazard explained

- How to pick the 4 funding periods

- Why funding market beats DeFi yields — the hub

Disclosure: I’m the developer of Yieldsforge. Simulation uses 2026 empirical means + volatility, randomly sampled. Not investment advice.